The British Pound has faced troubled waters since Brexit began to look like a reality. Theresa May was once again unable to find supporters for her plan. Lack of consensus sent the British Pound more than 100 points lower and knocked me out of a premature long position. Of course, the early long position was established on what would've been the greenest shoots of a breakout rally. I intended to add on to this position. However, risk control knocked me out at the week's low and suggested I establish a new, long position in the British Pound based on seasonal strength, in the near future.

The British Pound has moved slightly higher over the last few months. The rally has developed a manageable upward trendline, which was tested at Thursday's low of 1.3085. The market has consolidated over the last couple of weeks as we've drawn closer to actionable Brexit dates. Open interest has shrunk in the British Pound futures, and the total commercial position is its smallest since last April. Given the recent consolidation and drawdown in volume, we felt that most of the bad news is baked in, and any good news on the Brexit front could have sent the market above the 1.34 breakout level we've been watching before we could get our seasonal positions purchased.

Here's the information on the trade and our expectations. We'll update this trade idea with the real-time buy and sell signals, along with the protective stop prices in our nightly seasonal newsletter.

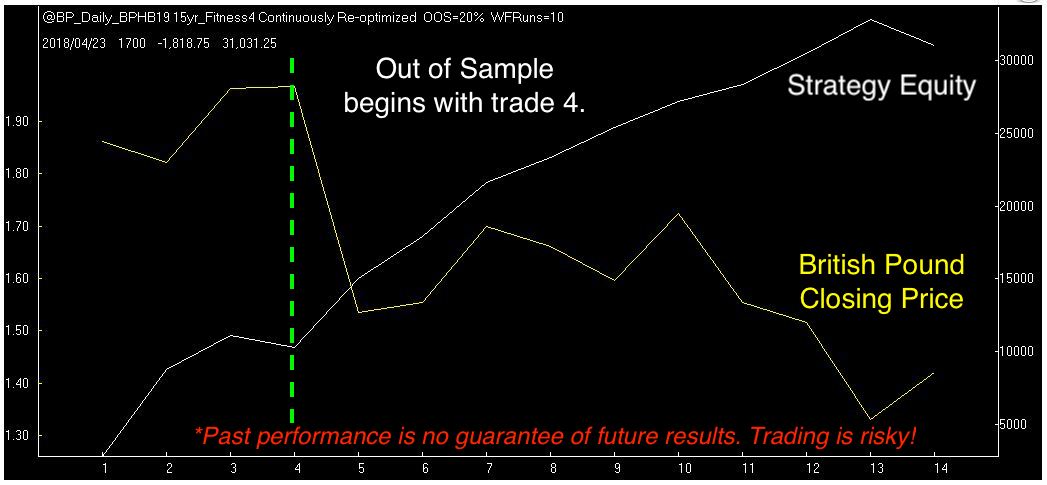

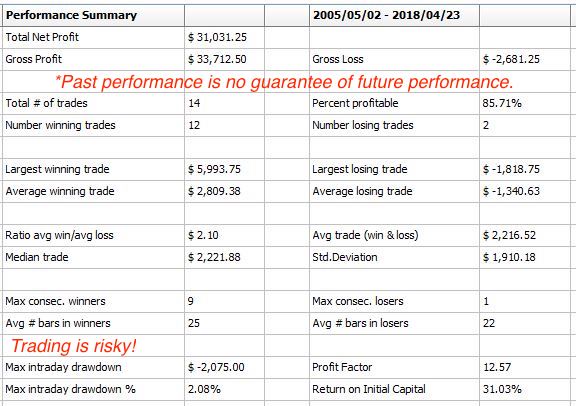

My chart plotting options are a bit limited but, the British Pound futures' closing price is plotted in yellow and has had a roughly downward sloping trend while the closed trade equity of the model we're using is plotted in white. Note that we begin the out of sample equity with trade number, 4. That means that last year's trade, which lost just over $2k has been the only loser in the series.

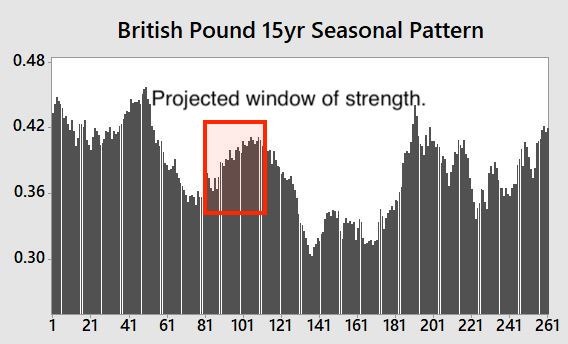

The window highlighted in our 15-year seasonal analysis, above, has produced the following out of sample results, below.

We'll be buying the June British Pound, shortly. Our readers will be prepared with a proper risk assessment. They'll know exactly where to place their protective sell stop, and when to get out. Casual observers can use the Monte Carlo results below, to get an idea for variance and mean return.

We set our Monte Carlo simulation to run 1,000 tests at $100,000. The mean average return is nearly four times the size of the standard deviation. This multiple suggests good odds that a winning trade will be significantly profitable. Setting the account size to $100,000 also makes it simple to translate the Monte Carlo results into a market forecast. The expected outcome at the end of our holding period is a close of 1.3371 +/-.068. Or, stated another way, there's a two-thirds chance that, if we're right, the British Pound will climb between 182 and 339 points during our holding period.

Please, let us know which phrasing makes more sense to you, the reader. I respect the time you're taking to read my work, and I'd like to make it as efficient as possible for all of us.