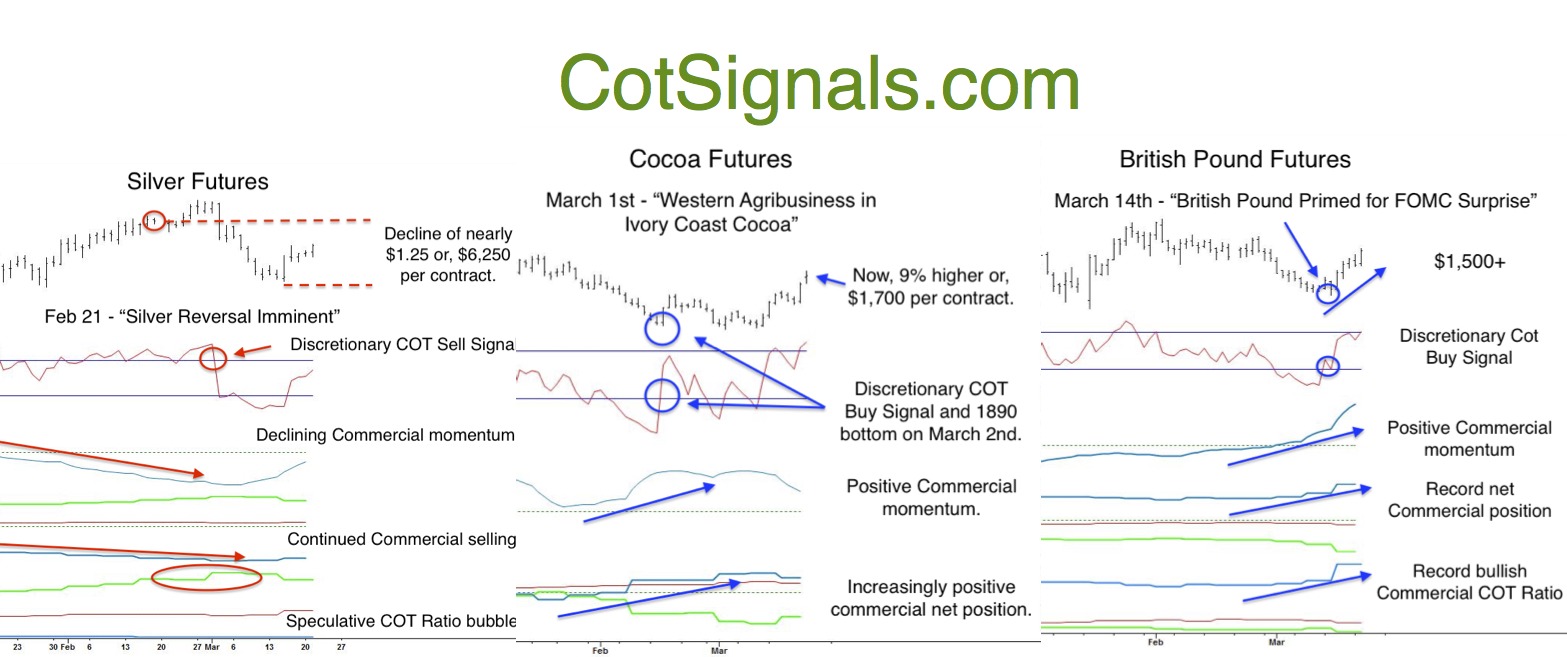

The Commitments of Traders(COT) report is the primary focus of our research. This weekly report published by the Commodity Futures Trading Commission(CFTC) details the actions of the commodity markets' three main participants; the commercials, large speculators, and non-reportables. We track the battle between the commercial traders and the large speculators. The commercial traders are the people who have a physical relationship with the commodity market in question while the large speculators are exactly what the name implies. There's an adage in the commodity markets along the lines of, "90% of speculators lose money in commodities." Our analysis has repeatedly shown that the large speculators have their most significant positions on at the most inopportune moments. We track these speculative bubbles and capitalize on their collapse. Please read on to see how this played out in our recent calls in the silver, cocoa and British Pound futures markets.

Our method is simple but, effective. First, we only take trades in the same direction as the commercial traders. We want to be buyers when they're buying and sellers when they're selling. The commercial traders are value traders. The collective intensity of their actions as gauged through their net and total positions helps us determine how sensitive their production or, consumption needs are at a given market price. In the case of the British Pound, commercial traders just set a net long record position. This is the kind of information we want to know and momentum we want on our side.

![COT Free Trial[1] copy](https://waldocktrading.com/wp-content/uploads/2016/09/COT-Free-Trial1-copy.jpg) Second, we manage risk. This is a swing trading or, mean version methodology. Our goal is to identify turning points that become profitable as a market reverses and the large speculators are forced out of the market. We define the criteria as a market in conflict. A market in conflict is overextended against the commercial traders' collective position in both price and the COT Ratio. This shows up on the charts as an oversold market in the face of positive commercial momentum in the case of cocoa and the British Pound. This manifests itself in the silver market as an overbought market in the face of a negative commercial outlook.

Second, we manage risk. This is a swing trading or, mean version methodology. Our goal is to identify turning points that become profitable as a market reverses and the large speculators are forced out of the market. We define the criteria as a market in conflict. A market in conflict is overextended against the commercial traders' collective position in both price and the COT Ratio. This shows up on the charts as an oversold market in the face of positive commercial momentum in the case of cocoa and the British Pound. This manifests itself in the silver market as an overbought market in the face of a negative commercial outlook.

Finally, the Discretionary Cot trading signals are triggered upon a reversal in the underlying market. The reversal provides two key pieces of information. First, it marks a change in direction. This helps us avoid catching a falling knife, etc. Secondly, the corresponding swing high or low that is created by the reversal provides us with a measurable protective stop placement point, which then tells us how many contracts to trade.

The key to the robustness of this application is that we base our actions on the consensus of the top agribusiness minds in the world. Whether we're discussing Nestle(NESN) stockpiling cocoa reserves at decade lows or Silver Wheaton(SLW) selling anticipated forward production, we want to side with the premier players. Adding a bit of common sense and some proprietary math and we have both a risk adjusted, fundamental method as well as a mechanical strategy for trading the commodity markets.