We have a seasonal trade coming in the April gold futures any day, now. Our seasonal approach is a bit different than most in that we go beyond determining seasonal bias and create a thoroughly thought out trade, including a realistic risk to reward profile.

Gold tends to exhibit a broad trend higher through spring. We'll be playing the early part of this move because it tends to be the most predictable. That being said, trading is never that predictable. Therefore, only true risk capital should be used. In this case, I'll be risking two percent from gold's opening price. That's about $2,630 per contract with gold trading at $1,315 per ounce.

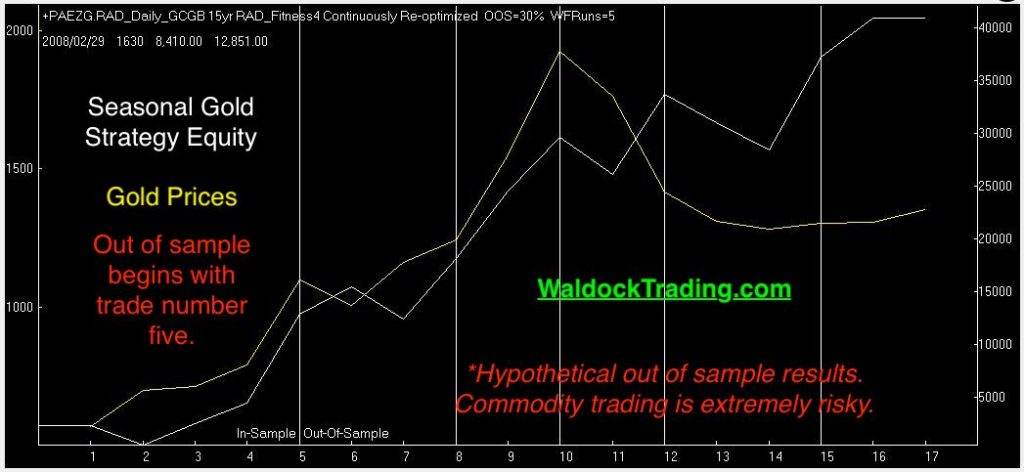

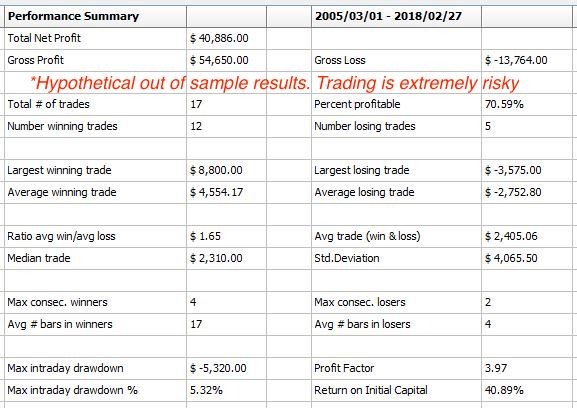

The out of sample performance report is below. Remember, every seasonal trade I place is hypothetical because I build a new model for each annual episode. You can see the results from our seasonal trade recommendations on our site.

As always, I supplement the performance results with Monte Carlo simulations. The sample size adjustment provides a fuller picture of what to expect if given enough opportunities.

The out of sample performance shows that we've only had two consecutive losing trades., and that's true. However, it's only valid for the given pass of data. Monte Carlo testing shows that over a 1,000 trade sample size, we could have four consecutive losing trades. Furthermore, it shows an average winning trade of more than $4,500. Placed in context, this really means that gold was trading at higher, more volatile prices in the past. Translating the mean average return of 2.3% to today's price suggests an expectation nearer $3,000.

Finally, for those of you trading gold exchange-traded funds or notes, Monte Carlo testing via ratio adjusted historical contracts and a $100k account balance, allows you to see if the move is significant enough to merit the extra seasonal allocation to boost your returns at this critical cyclical moment.

Sign up, and we'll notify you when it's time to trade, the margin required, where to place your protective stop loss order and, hopefully, when to take profits in roughly twenty days.