The fundamentals in crude oil have continued to erode since February of this year. The highs, over the last $40, can be viewed as a “bubble.” This bubble has been fueled neither by Commodity Index Traders and large speculators, nor Hedge funds and carry trades. I think a strong case can be made that the last leg of this rally should be attributed to large producers unwinding their forward hedges. Producers and forward short hedgers are subject to human error just as individual traders are. Hedge transactions manifest themselves in the Commitment of Traders data as commercial purchases when the market makes new lows and as commercial sales when the market rallies. Just as most economic decisions are made, “at the margin,” so too are the hedger’s trading decisions. Their traders use their understanding of the fundamentals in their market to create oversold and overbought zones within the market’s natural movement and attempt to trade accordingly.

This strategy works for them the vast majority of the time. However, when a market unhinges from fundamental factors and begins trading on sentiment, the commercials find themselves at the mercy of the public at large. Using the chart below, the white line represents the commercial index of positions on a scale of 0 to 100. Zero equals totally short and can be seen at the following points, (5/06, 7/07, 8/07). One hundred equals totally long and can be seen at, 6/05 and 10/05. Currently, the index is at 78, the highest since a 79 reading in February of ’07.

The yellow line represents total open interest. Technically, speaking, in a healthy trend, open interest should increase as the market moves out to new territory, either higher or, lower. This has not been the case with crude oil. Open interest peaked in July of ’07 and has continued to decline ever since. Open interest now stands at 1.3 million contracts, the lowest since March of ’07.

Furthermore, I have discussed, at length, the negative spread we’ve seen between the front month prices and the later expirations. In real terms, this backwardation in prices is evidence that producers don’t believe that we will be near these prices as the deferred contracts come due for delivery. Producers continued to sell the deferred contracts in order to lock in profits at levels they don’t believe will hold into the future.

Lastly, over the last previous weeks, we have seen the total commercial position shift from net short, to net long, with the market at all time highs. Therefore, I would suggest that the rally from the January highs, under $100 per barrel through the current highs, over $145 has been driven by commercial capitulation and a speculative blow off, rather than fundamental supply and demand issues. Ultimately, it proves the old adage true for everyone, even the big guys, “The market can remain irrational longer than one can remain solvent.”

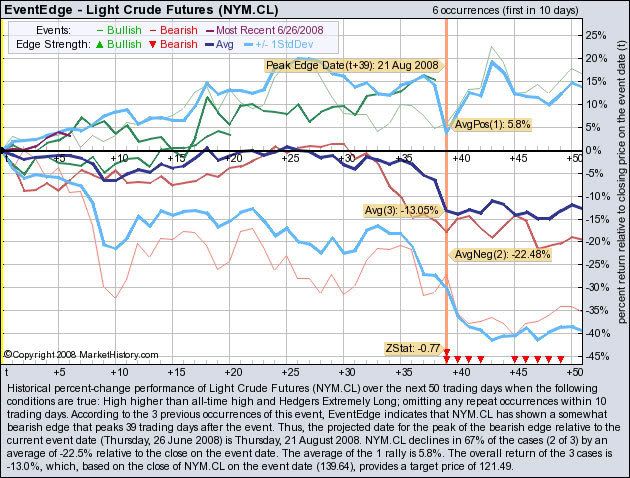

Historically, there have only been three times when commercial positions have shifted from net short, to net long while the market was at all time highs. The market declined, twice, by an average of 22.5% and once, the market rallied by 5.8%. Clearly, we are on the cusp of a top. Given the magnitude of a possible decline, one may be advised to purchase put options. Those wishing to sell futures may wish to wait for a close under $140 to initiate a short position.